by

by Homeowners insurance is a crucial safety net, protecting your most valuable asset. However, many people are surprised to discover that their policy doesn’t cover everything they assume it does. Understanding these gaps in coverage can save you from unexpected financial burdens down the line. Let’s explore some common exclusions.

Flooding

Most standard homeowners insurance policies explicitly exclude flood damage. Flooding is usually covered under a separate flood insurance policy, often provided by the National Flood Insurance Program (NFIP). If you live in a high-risk flood zone, purchasing a separate flood insurance policy is crucial.  Don’t assume your home is safe; even a small amount of water can cause significant damage. Learn more about flood insurance options.

Don’t assume your home is safe; even a small amount of water can cause significant damage. Learn more about flood insurance options.

Earthquakes

Similar to flood insurance, earthquake coverage is typically a separate add-on to your standard homeowners insurance policy. Earthquake damage can be catastrophic, resulting in extensive structural damage and personal property loss. If you live in an earthquake-prone region, consider adding this crucial coverage to your policy.  The cost of repairing earthquake damage can quickly exceed your financial capacity without this specific coverage.

The cost of repairing earthquake damage can quickly exceed your financial capacity without this specific coverage.

Pest Infestations

While your insurance might cover sudden and accidental damage from pests, it usually doesn’t cover the costs associated with long-term infestations like termites or carpenter ants. These infestations can cause significant structural damage over time. Regular pest inspections and preventative measures can help mitigate the risk, but won’t completely eliminate it. Check out preventative tips from pest control experts. Ignoring these issues can lead to a much bigger problem later.

Neglect or Lack of Maintenance

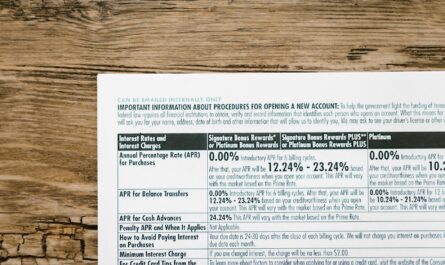

Damage resulting from your neglect or failure to maintain your property is generally not covered. This includes things like a leaky roof left unrepaired, leading to significant water damage. Regular maintenance, such as annual roof inspections and gutter cleaning, can prevent costly repairs and potential insurance disputes. Read our guide to home maintenance. [IMAGE_3_HERE] Taking proactive steps is crucial to avoiding these kinds of issues.

Acts of War or Terrorism

Most homeowners insurance policies exclude damage caused by acts of war or terrorism. These events are typically covered under different specialized insurance policies. These are unpredictable events, but awareness is key in understanding your policy’s limitations. This is often overlooked, and it’s important to understand what your policy will and won’t cover in a major event. Learn about the complexities of war and terrorism insurance.

Conclusion

Understanding the limitations of your homeowners insurance is just as important as understanding its coverage. By being aware of these exclusions, you can take proactive steps to protect yourself and your property from unexpected financial burdens. Remember to review your policy regularly and ask questions if anything is unclear. Contact us to review your policy today.

Frequently Asked Questions

What if a tree falls on my house? This depends on the cause. If it’s due to a sudden and unforeseen event like a storm, it’s likely covered. However, if the tree was already rotting and you failed to address it, it might not be.

Does my insurance cover mold? Mold coverage varies greatly depending on the cause and extent of the damage. Often, coverage only applies if the mold is a result of a covered event, such as a burst pipe. Consult your insurance provider for details.

What about damage from a power surge? Damage from a power surge may or may not be covered depending on your policy. It often requires an additional rider to your coverage.

Can I get additional coverage for these exclusions? Yes, you can often purchase riders or supplemental insurance to cover many of these exclusions, such as flood or earthquake insurance. It is highly recommended to add these if you live in a high-risk area.